The Transportation Comeback: A Market Turning, Not Yet Recovered

Over the past few years, the transportation and logistics sector has operated in one of the most challenging environments in recent memory. What began as a post-COVID normalization quickly turned into a prolonged freight recession, marked by excess capacity, softening demand, and sustained pressure on rates. For many operators, particularly small and mid-sized carriers, the past two years have been less about growth and more about survival.

Early Signs of a Recovery Are Taking Hold

As we move through 2026, there are increasingly clear signs that the market is turning.

The recovery is not uniform, and it is certainly not complete. Yet across the industry, conversations have shifted. Lenders who had pulled back are re-engaging. Industry associations are expressing cautious optimism. Operators who spent the last two years cutting costs are beginning to talk again about positioning for growth.

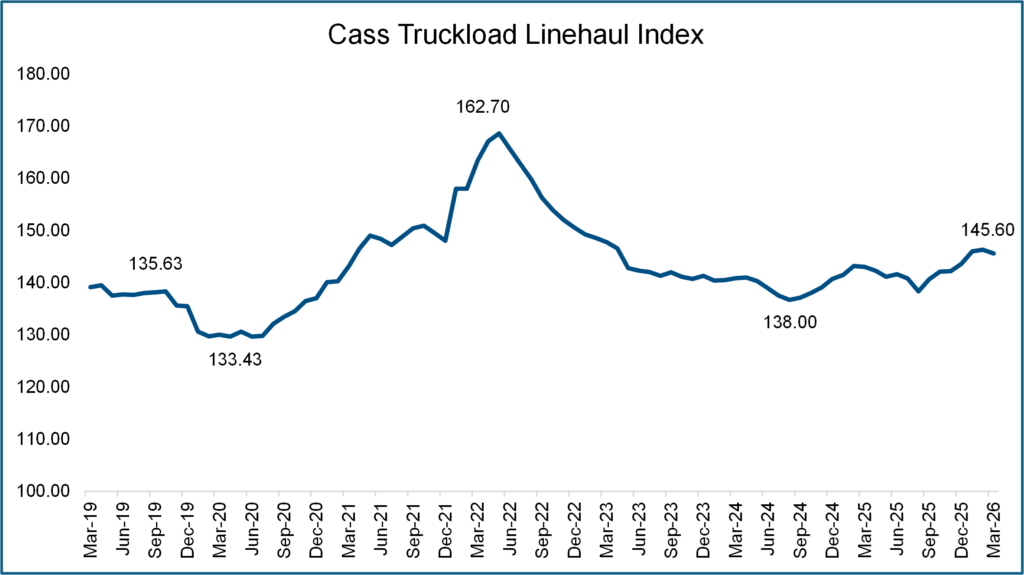

Part of this shift is showing up in the data. Spot rates, which were under significant pressure throughout 2023 and much of 2024, have begun to move higher. In many lanes, rates are meaningfully above prior-year levels, and contract pricing has started to follow.

Source: Cass Truckload Linehaul Index

Definition: The Cass Truckload Linehaul Index is an accurate, timely indicator of market fluctuations in per-mile dry van truckload pricing in the U.S. The index isolates the linehaul component of full truckload costs from other components (e.g. fuel and accessorials), providing an accurate reflection of trends in baseline truckload prices.

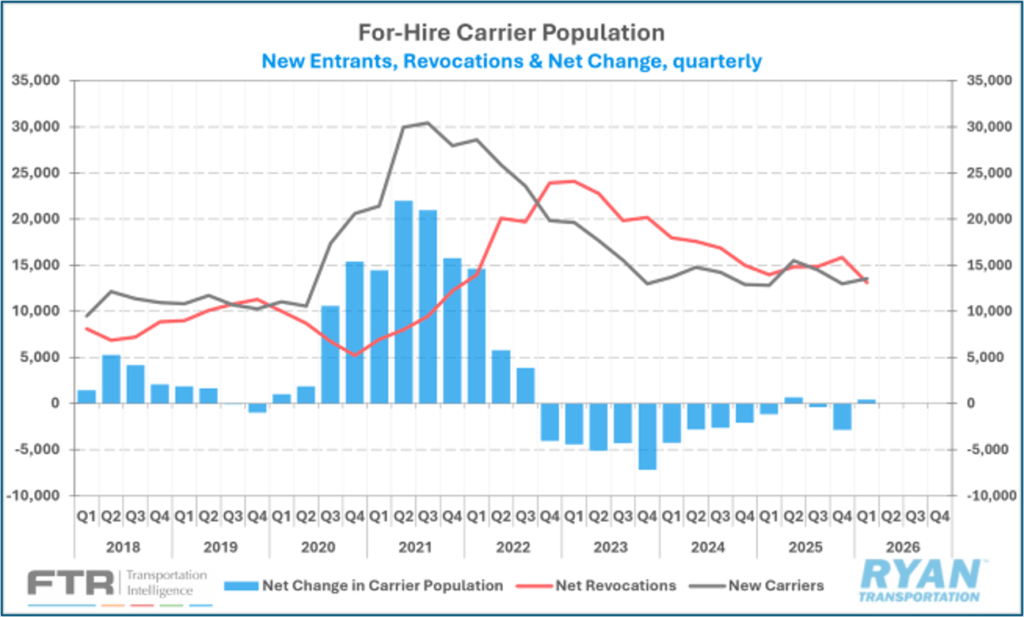

While volumes remain uneven, the supply-demand imbalance that defined the downturn is beginning to normalize as capacity exits the system. Thousands of carriers that entered the market during the peak have since disappeared, and with them, a significant amount of excess supply.

This is not a demand-driven recovery, at least not yet. It is, more accurately, a margin recovery. Pricing is improving not because freight volumes have surged, but because the market has finally worked through its oversupply. For operators who have weathered the downturn, that distinction matters. It means profitability can return even in the absence of strong top-line growth.

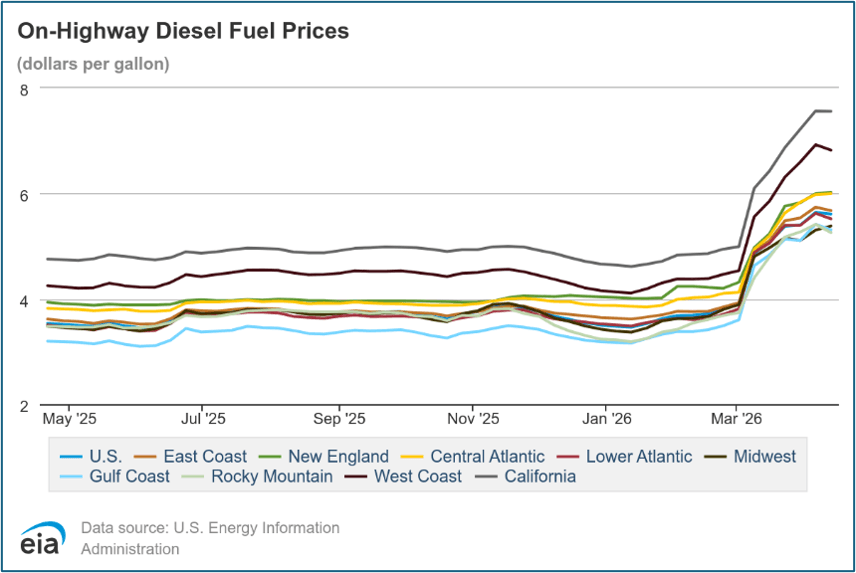

Fuel Volatility Is Re-Entering the Equation

Recent geopolitical developments have introduced renewed volatility into energy markets, with diesel prices moving sharply higher in a short period of time. Fuel has always been one of the largest cost components for carriers, but in a low-margin environment, even modest increases can have an outsized impact. What makes this cycle different is that many carriers are better positioned to manage that volatility than they were in the past.

Fuel surcharge mechanisms, long a standard feature in transportation contracts, are taking on renewed importance. In prior years, particularly during periods of weak demand, carriers often absorbed fuel increases in order to remain competitive. Today, as capacity tightens and pricing power improves, those same carriers are more disciplined in enforcing surcharge structures. The result is a more effective pass-through of fuel costs to shippers, which helps preserve margins and stabilize cash flow in an otherwise uncertain environment.

That shift is subtle but meaningful. It reflects a broader change in market dynamics, where carriers are beginning to regain leverage after an extended period of shipper-driven pricing. It also creates a clearer line of sight into operating performance, something that has been difficult to achieve over the past several years.

Implications for M&A and ESOP Activity

Periods like this where the market is stabilizing but valuations have not yet fully reset upward have historically created opportunities. Stronger operators, having survived the downturn, are often in a position to expand. At the same time, many business owners who have endured the volatility of the past few years are reevaluating their long-term plans. For some, that means considering a sale or recapitalization. For others, it means exploring alternative ownership structures that provide liquidity while preserving independence.

Employee ownership, in particular, continues to gain traction in this environment. In an industry defined by labor challenges and cyclical performance, ESOPs offer a path to liquidity that does not rely on perfect market timing or a single buyer outcome. They can also provide a framework for retaining and incentivizing employees at a time when talent remains a critical constraint.

More broadly, there is an increasing focus on capital structure. The past two years have underscored how quickly conditions can change and how important flexibility can be. Whether through traditional M&A, minority recapitalizations, or ESOP transactions, companies are thinking more deliberately about how they position their balance sheets for the next cycle.

None of this suggests that the industry has fully recovered. Freight volumes remain inconsistent, and macroeconomic uncertainty has not disappeared. But the conversation has clearly shifted from contraction to stabilization, and in some cases, to opportunity.

For owners and leadership teams, that shift matters. M&A markets do not wait for perfect conditions. They respond to inflection points; moments when the direction of travel becomes clearer, even if the destination is not fully defined.

The transportation sector appears to be entering one of those moments now.

The question is not whether the past two years were difficult. That is well understood. The more important question is what comes next, and whether companies are positioned to take advantage of a market that, while not fully recovered, is no longer in decline.

ADDITIONAL RESOURCES